By Bhvita Jani

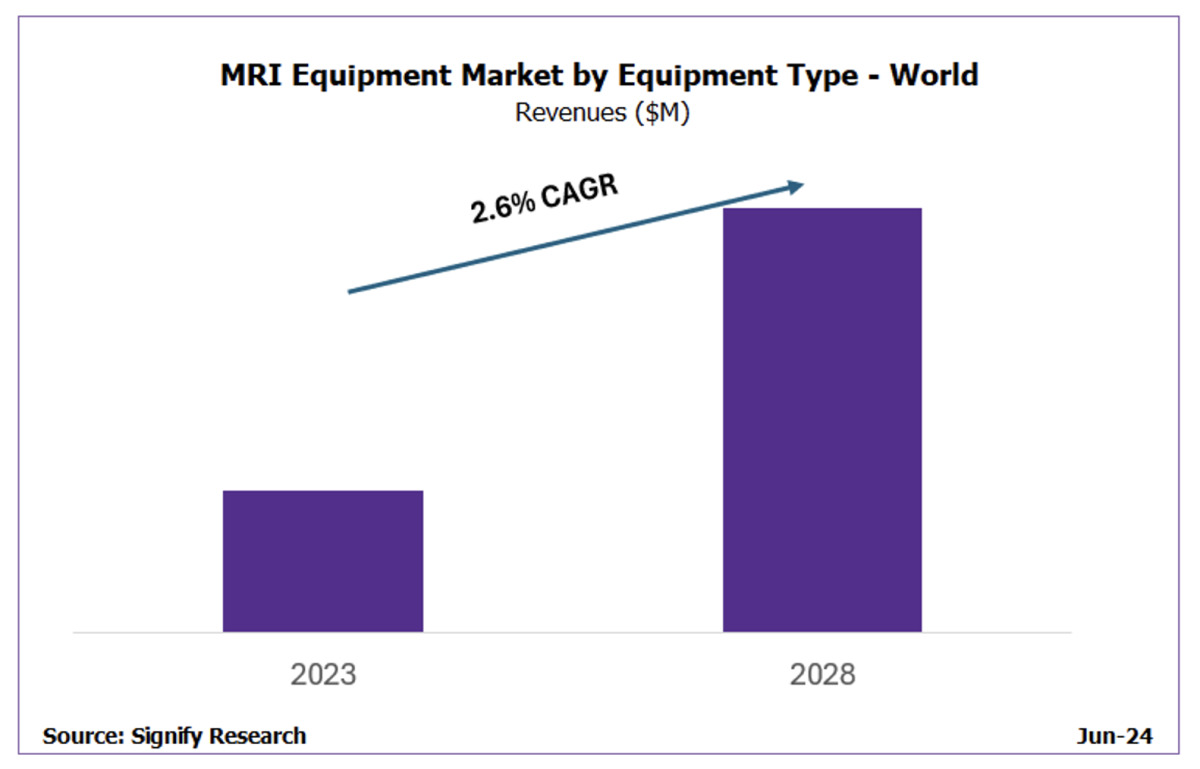

In 2023, the MR equipment market experienced an impressive 11.8% year-over-year revenue growth. This surge was largely driven by pent-up demand resulting in record order books in addition to inflationary pressures that drove pricing upwards. In Western Europe, a robust recovery during this period was propelled by increased public spending on post-COVID service line improvements and the satisfaction of pent-up demand. Furthermore, the easing of supply chain challenges resulted in shorter lead times for MR installations.

Unit shipments reached over 6,300 in 2023 and are set to exceed 7,400 by 2028. However, healthcare providers continue to contend with workforce shortages, highlighting the urgent need for more streamlined workflows to manage the growing backlog of MR procedures.

Ad Statistics

Times Displayed: 364749

Times Visited: 21098 MIT labs, experts in Multi-Vendor component level repair of: MRI Coils, RF amplifiers, Gradient Amplifiers Contrast Media Injectors. System repairs, sub-assembly repairs, component level repairs, refurbish/calibrate. info@mitlabsusa.com/+1 (305) 470-8013

The market is anticipated to rebalance in 2024 after a particularly strong 2023. As such, the outlook for 2024 seems weaker due to rising political risks in the U.S. and global macroeconomic uncertainties. By late 2023 to early 2024, the pent-up demand caused by COVID-related supply chain issues is projected to diminish, with record order books returning to more typical levels. In contrast, China is expected to see a market rebound and recovery.

Clinical trends propelling the MR market

Alzheimers:

New U.S. funding for research into Alzheimer's and other neurodegenerative diseases is boosting MR demand. The Leqembi drug trial uses MR screening to monitor side effects and disease progression. With pharmaceutical companies focusing on neuro MR, mid-term demand is expected to rise, sustaining the premium U.S. market. However, the lower image quality of the recent ultralow frequency (ULF) market developments limits uptake. Additionally, artificial intelligence (AI)'s maturation for stroke triage drives investment in new MR-based AI tools for neurology.

Prostrate:

MR for prostate screening is gaining traction, driven by studies comparing it to prostate-specific antigen (PSA) testing, which is subsequently influencing European guidelines. New AI tools like Cortechs.ai, Saige (DeepHealth), and Lucida Medical are improving diagnosis and reporting by utilising real-world evidence. However, adoption is hindered by limited screening programs, inadequate funding for prostate AI, and lack of reimbursement. The high MR costs versus PSA tests remains a barrier. Stronger evidence on patient outcomes and return on investment (ROI) is crucial for broader acceptance. A patient-driven "out of pocket" model, akin to RadNet ECBD, may emerge if payers are hesitant.